SECTION A:

The tennis and pickleball clubs contributed club funds to pay for community awnings at the HOA sports center. The Board took these monies from the clubs in mid-April 2020. The background of this scheme is detailed below in Section B. After the Board took these monies, the president of the pickleball club expected the Board to vote a certain way at the May 7, 2020 Board meeting in what appeared to be a quid pro quo expectation. When they did not so vote, later that afternoon she sent the following email to the Board which she then forwarded to the entire pickleball club. We leave it to the readers to judge for themselves the appropriateness or lack thereof of this email to the Board.

Here is the email from Diane Fiorillo Green on behalf of the Pickleball leadership team to the entire pickleball club urging the membership to vote out the encumbent Board members at the next election cycle. We have highlighted in red some salient parts of this letter.

Hello Pickleball Members,

In an effort to keep communication lines open, the following letter was submitted to the board in response to our presentation at the Board meeting yesterday.

Thank you

Pickleball Leadership Team

President: Diane Fiorillo Green

Vice President: Donna Moreau

Communications: Sue Leonard

Secretary: Debbie Ganguzza

Treasurer: Robin Day-Schmierer

Dear Board Members,

We are writing to you today as we needed to simmer down a little while after the HOA Board Meeting yesterday. We are so disappointed and disillusioned by the members of the Board with the exception of Sue Schmer who, to her word, was prepared with accurate information and listened with an open mind. What happened to the vote?

Both Pickleball and Tennis were invited to speak on behalf of our members requesting the opening of the tennis and pickleball courts in line with the directive from Governor DeSantis in April to start opening recreational facilities. What we all had to listen to prior to our presentation left us speechless. Please see link for clarification.

It was blatantly apparent the vendor portion of the meeting, cleverly positioned prior to our presentations, was orchestrated to push and agenda – an agenda to keep our facilities closed. Let’s be honest, the vendors had a lot to say but little in relevance creating more unnecessary fearmongering with their unscientific rhetoric and outright lies.

First, both venders stated that there were no communities open or opening and that is simply not true. The truth is that Rainberry Bay, a community that First Service manages, is open. The truth is that several Cascade Lakes’ residents have played next door at Indian Springs. The truth is that the communities listed by Pickleball are open and others have dates to open. All of this information was verified by Lee & Perry Sinett and provided to the board prior to the meeting. In addition, our members have personally heard from residents that a Board member is telling people that we lied and that those communities are not open. We are deeply disappointed and outraged by this level of deceit.

Second, our Board president stated that the directive being discussed was the same as a stage one opening in our state in which Palm Beach County has been excluded. This is simply another lie. The unscientific and unsubstantiated ramblings of the pool vender isn’t worthy of further note. That was addressed brilliantly by resident epidemiologist, Dr. Jeff Hymen. See link:

We want our courts to open and we want it done safely. There is a plan provided by Lee Sinett, and it can be executed within 48 hours. You can choose today after speaking with the attorney to open the courts.

The lack of board action is making the community at large divisive, and that’s not healthy. Not opening the courts is a discriminating action against the active members of this community. That is a brave stance to take. It will be remembered.

It will be remembered during election time when we get to vote and elect four new board members. It be remembered that it was Pickleball and Tennis that helped the board out of a bind just two weeks ago when we furnished funds for a botched tennis canopy purchase. It will be remembered that we are putting in sweat and equity and running committees to serve the community. Tennis and Pickleball are united on this issue and that is a formidable force.

The Pickleball Leadership team.

|

May 22, 2020:

Update:

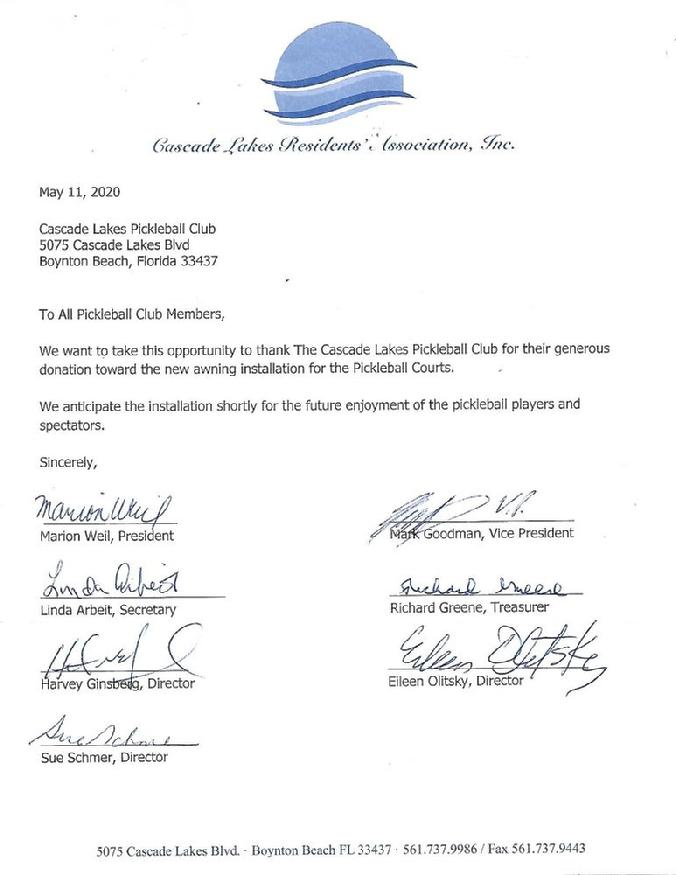

The Board sent a letter dated May 11, 2020 addressed to "All Pickleball Club Members" and apparently mailed it to the clubhouse address, which is where it emanated from to begin with (so why mail it?). This letter was then emailed to the pickleball club members on May 22, 2020 by someone who has access to the HOA website's club mailing list. This letter from the Board thanked the pickleball club for their “donation” toward the awning purchase (see below). This letter was dated a mere 4 days after the president of the pickleball club’s scathing email to the Board condemning them for not permitting limited play on the courts and warning them that their actions would have consequences come election time (see above). This “thank you” letter from the Board is a clear attempt to pacify and assuage the pickleball club members solely to retain power and dampen the effects of their widely derided decision concerning court play.

How do we know this? Because it was written a mere four days after the condemning email from Diane Green referenced above, and it was not written for over a month since the taking of the monies.

|

May 24, 2020:

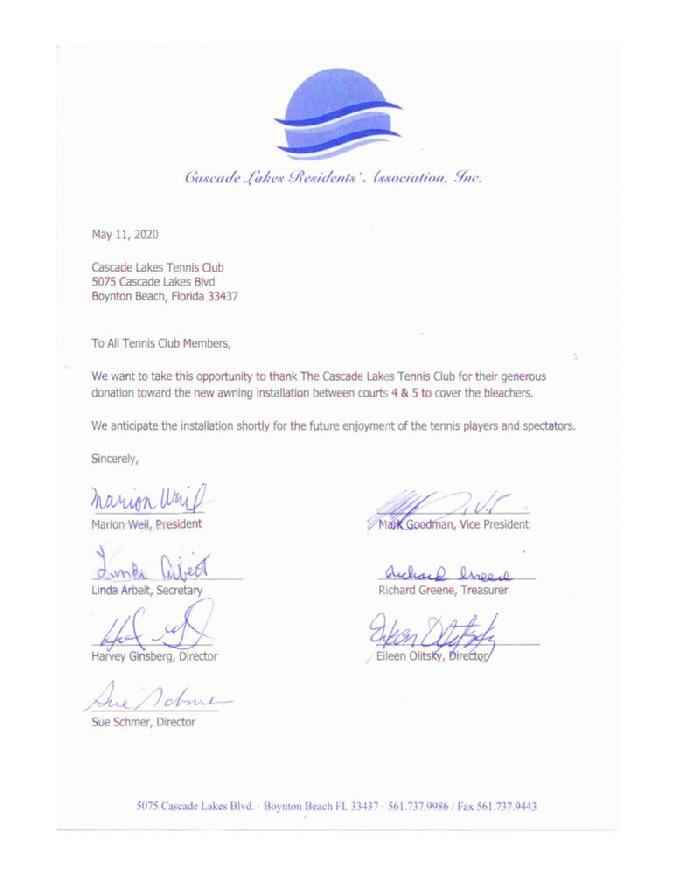

The tennis club's communication officer sent out an email with the Board’s thank you note to them contained therein. There was no message; just an email from the HOA website’s email list to the tennis club membership with the Board’s letter. Here is the entire text of that email:

On May 24, 2020 3:33 PM Patricia Nast <noreply@cascadelakeshoa.net> wrote:

|

In response, at 3:51pm, your Editor and Roving Reporter sent the following email to Pat Nast, Communication Officer of the Tennis Club:

“Hi, Pat,

A couple of important questions to clarify the record.

1. When exactly did any officer of the tennis club receive the letter from the Board? Was it just received today for the first time?

2. Can you please forward to us the original email from the Board with the letter attached?

Thanks,

Vicki Roberts and Arthur Andelson”

We also left a voicemail to Pat on her cell phone.

At 7:19pm we received the following email from Pat:

“The letter from the board was sent via the post office. It arrived either Thursday or Friday. There is no email to forward to you.

Pat”

This raises more questions:

1. Why would the Board use the postal service and send via snail mail a letter to the clubs addressed to the clubhouse office address, which is where it emanated from to begin with (so why mail it?), and which is not the address of record of either of the two clubs? For the record, and as an example, the Florida Department of State lists the pickleball club’s official corporate address as 5386 LANDON CIRCLE BOYNTON BEACH, FL 33437 which is the pickleball club treasurer Robin Day-Schmierer’s address, and specifically not the clubhouse address;

2. Why would the Board send the letters to the closed clubhouse where someone would have to expose themselves to others during a pandemic in order to retrieve them?

3. Who picked up the letters?

4. Why didn’t the Board email the entire HOA membership as it does with many community-wide notices?

5. What Board member decided to send out these letters almost a month later and why?

The entire way this matter was handled from the beginning was an abomination as previously detailed on this news site; these letters went weeks after the Board voted to accept club moneys for an HOA improvement on April 16, 2020, and clearly went out on May 11, 2020 in response to the scathing email sent by Diane a mere four days earlier, wherein she demanded or was expecting a quid pro quo for the pickleball club’s “donation.” The timing of the letters is noteworthy (Diane’s email was dated May 7th; these letters were dated May 11th).

|

SECTION B:

AWNING, PAVERS, FENCE

INTRODUCTION:

The issues concerning the awning between tennis courts 4 and 5 as well as the pavers and the fence are troubling, and they will cost this community substantial funds if they are not addressed. The quick fix proposed by the Pickleball and Tennis Clubs’ leadership does not resolve the problems and is an improper use of club funds.

There is a huge safety hazard right now at the location. These issues are so important that we have devoted a designated page to review all of them, and we urge our readers to read all of it, so that there are no surprises in the future when the community is hit with a lawsuit from an accident waiting to happen.

Fawning Over An Awning, Part One:

April 6, 2020:

The Pickleball and Tennis Club leadership sent out concurrent email blasts advising the members of their unilateral decision to spend club funds for corrective awnings ($1,000 and $2,000 respectively).

The Pickleball Club and Tennis Club leadership have no authority to spend club funds without a membership vote. It is also completely contrary to the Pickleball Club’s bylaws on file with the State of Florida.

Both your Editor and your Roving Reporter are members in each of these clubs and we object to our money being spent without our permission.

If there is an awning issue, it is for the Board to rectify after the leadership teams have brought the issue to the Recreation Committee.

The entire HOA is responsible for the common areas, and no club money should be spent for any purpose which enhances a common area.

Fawning Over an Awning, Part Deux

April 8, 2020:

The Tennis Club leadership sent an email to the tennis club members urging them to vote yes to spend club money for a corrective awning after the one approved by the HOA apparently was defective in some manner. This email made statements which were, in the opinion of many, skewed and unfair, and only occurred because they had to be reminded that this expenditure required a club membership vote.

Here is that email in its entirety:

“This is an important message about the awning between Courts 4 & 5.

It has been brought to our attention that the tennis club must vote for use of funds over $500. So we are asking all of you to get back to us with your answer. These are strange times, and an unusual circumstance. We want to expedite things without losing the deposit on the awning. The wrong size came in and was returned to the vendor, and we need to move forward if we want to use our deposit for the correct one. It’s complicated – let’s not get caught up in whose fault it is, but try to keep an eye on our goal and move forward.

Let’s focus on OUR project – we are not dependent on what the other club is doing. This is something all of us in the tennis club have wanted for a long time – why would we not want to proceed with completing the project? We have proposed putting in $2000, which is less than 25% of the total cost. The $2500 deposit placed on the original order will then be applied to our awning. The remainder will be provided by the community. It is a good investment – as we discussed at our last meeting, we want to start using funds for things to improve the tennis facility. And it’s for completing what has already been underway. We have all agreed in the past that we want this awning.

Doing this will generate tremendous goodwill with our HOA board and will pave the way for future items we will be asking them for. We will get our investment back, and more.

Goodwill and getting along with our neighbors – something to strive for, especially in these difficult times. We were hoping that making a unified front could be a way of offering the olive branch and start acting like we are a group of people who consider the greater benefit of the community we belong to. We are all neighbors, after all.

So what do you say? Please respond by Friday @ Noon: to ritalindy1112@gmail.com or reply to this email. Couples who are both members can respond with 2 votes in a single email.

YES – I want the tennis club to contribute $2000. Doing so is a vote of goodwill and faith in our future.

NO – I do not want the tennis club to contribute. Keep in mind that this means losing the $2500 deposit, which is YOUR money also – it comes out of your HOA dues.

Thank-you for your time and have a happy holiday!

The Tennis Club Board Members”

Your Editor sent the following email back in response:

“Good will toward our HOA board? They serve us, not the other way around. Respectfully, you have it backwards.

Honestly, the way your email is skewed is extremely disappointing. The sports center area is a common area and is the responsibility of the HOA, not the clubs.

If the vendor screwed up, then the vendor is required to return all funds and the HOA should start again with a new vendor or the original vendor needs to correct its error. This is a no brainer.

Cordially,

Vicki Roberts”

Fawning Over an Awning, Part Three:

The Pickleball Club Leadership then sent an equally manipulative email to its membership through its No-Reply email blast, reprinted here in its entirety:

“Pickleball Members,

An opportunity (subject to BOD approval) presented itself to the Pickleball Club to obtain a canopy for the pickleball courts at a significantly reduced rate. This proposal will enhance the uniformity and beauty of our shared outdoor sports facility. Our contribution as a club would be only $1000. from our treasury.

Both the Pickleball Club officers and the Tennis Club officers have decided to put the proposal of the canopies to a vote of their respective members.

All Pickleball Club members are encouraged to vote.

Please vote by Friday 4/10/20 at 12 noon

Yes – I want the Pickleball Club to contribute $1000. Doing so is a vote of goodwill and faith in our future.

No – I do not want the Pickleball Club to contribute. I do not want the canopy.

Click the link below to cast your vote

CLICK HERE

| Sincerely, |

| Pickleball Leadership Team |

| President: Diane Fiorillo Green |

| Vice President: Donna Moreau |

| Communications: Sue Leonard |

| Treasurer: Robin Day Schmierer |

| Secretary: Debbie Ganguzza” |

Editor’s Comments:

This type of blatant manipulation is an insult to the community. The Yes/No choices have manipulative commentary following each.

Further, the officers did not “decide” to put the proposal to a membership vote: they were called out on their plan to spend club monies without a vote, and had to be educated on the impropriety of spending other people’s money without a vote.

I remind them that they have a fiduciary responsibility to safeguard those funds and I repeat the same admonition I gave to the tennis club leadership above.

SHODDY WORKMANSHIP EQUALS SAFETY HAZARD:

Your Roving Reporter Has This Additional Information which concerns the entire area:

Report Filed By Arthur Andelson:

There were only 3 things needed to improve the common area between tennis courts 4 and 5:

- Pavers to increase the viewing area by going around the bleachers’ cement slab as well as pavers for the walkway leading to the viewing area;

- A fence along the pavers walkway to avoid injuries due to the slope holding up the pavers; and

- An awning to shade the viewing area similar to the other awnings between other courts.

The BOD and Property Management struck out on all three. Not one part of the job was completed competently or with any forethought or oversight.

Part 1: The pavers in the viewing section were completed satisfactorily, however, the walkway pavers will not last very long and a “trip and fall” is waiting to happen. As mentioned before to the BOD and the Property Manager, there will be erosion and the outside bricks will begin to lift, sink, and wobble. There is only a half inch of cement under the dirt and that is already cracking and can be broken with a little pressure from a finger. The cement is already cracking and shifting at the top of the slope next to the pavers. At least 3 pavers are already loose and wobbly. This was brought to the attention of the BOD at the March 18, 2020 board meeting, at the Second Residents’ Input Session, which is reprinted here from the Synopsis and Commentary of that BOD meeting:

“Arthur Andelson: I have a question. The pavers between the tennis courts, it is a high slope. It’s sand. It will erode and the pavers will start to slip. When the guard rail is put in, will there be something put there -- railroad ties – or concrete, or something to shore up the sides?

Marion: we’ll ask our fence guy and ask him about that.

[Editor’s note: Arthur called our property manager, Deborah, this morning, March 19, 2020 to follow up on this issue. She advised him that when the fence people arrive to put in the post, she is aware that she may have to call back the paver installer to shore up the pavers.]”

None of this was taken care of and the situation has now become a hazard as shown in the below photos, which show the dangerous condition left by the installers of both the pavers and the fence.

Part 2: If the fence were placed in lower and closer to the pavers as compared to the fence on the walkway between courts 2 and 3, the lower railing would assist in holding the pavers in place with additional cement underneath the railing and between the railing and the pavers. Actually, the location where the loose pavers were noticed was caused by the manner in which the fence was put in the ground in the first place. This shoddy installation should have been rejected as being subpar and the installer should have been required to re-do the job properly.

Today’s photos show the dangerous conditions, including wobbly pavers, shifting slope, and erosion, all of which would not be a serious safety issue had there been properly installed pavers and a properly installed fence, which I warned about and for which my warning clearly went unheeded. This is a liability exposure and the more time that goes by, the more likely the HOA will have to pay to have this rectified instead of demanding that these jobs be completed properly by the vendors who were paid.

Part 3: Concerning the awning, during the Board meeting of February 19, 2020, the board voted to have matching awnings with the other bleacher viewing areas and to use the same awning company. So how can this job have been done incorrectly and why would the HOA be required to pay more?

CONCLUSION:

In conclusion, with regard to all of these issues, it is incumbent upon the Board and the Property Manager to fix these problems now, before they will have to be fixed later at additional cost and before there is an accident which will cost this community a heck of a lot more once that lawsuit is filed. The fact that the HOA and the Property Manager have been put on notice and failed to mitigate the dangerous condition means the HOA will be held liable. This should not cost the HOA any additional money if all of it is fixed now, since the vendors are responsible if the Board acts quickly. Those vendors should be licensed and bonded, so there is no reason that these issues should not be fixed by the vendors now, at no additional cost to the HOA.

Here are the photos which I took today which clearly show the problems detailed above:

|

April 11, 2020:

According to reports from the leadership teams, memberships of both clubs overwhelmingly voted “yes” to spend club funds on a common area improvement which is exclusively within the purview and responsibility of the HOA. It is lamentable that so many club members chose to ignore procedural formalities and the clear rules of this HOA. This vitiates the complaints many of you voice concerning how this community’s leadership functions. By doing this, you are endorsing this type of malfeasance.

Also remember that one does not have to be a club member to play on the courts; the clubs are now agreeing to subsidize the use of that common area for non-club members, the community at large, and their non-resident guests.

Further, the yes/no portion of both ballots was patently unfair and manipulative. For example, one might be in favor of the canopies for both areas, but then faced with the wording of the ballot, left in a dilemma because wanting the canopies was inconsistent with a “no” vote as phrased. One may believe that the screw-up should fall squarely on the HOA to negotiate and fix the problem, and still want the canopies.

It appears that the leadership teams of both clubs were so afraid that an honest and straight up “yes/no” vote would result in the clubs rejecting the proposal, that they worded the ballot in such a way as to insure its passage. If this is what you want in your leadership, then by all means vote for them again at election time.

It also appears that this exercise was meant to buy favoritism with the Board, as evidenced by the repeated claims that a ”yes” vote would be a vote of goodwill toward the Board. The Board represents the HOA members, and it owes fiduciary duties to the members. Sucking up to the Board in this blatant and embarrassing manner does not promote good will; rather, it promotes the exact type of wheeling and dealing that we have consistently called out as being a violation of the Board’s fiduciary duties to the entire HOA membership. It improperly promotes favoritism; that’s fine and dandy when it suits your purposes, but you may rue the day when it suits someone else’s purposes and you are left holding the bag.

In the meantime, it is obvious that the dues required for club membership are way too high, since apparently the clubs have thousands of dollars to spend on common area improvements, as opposed to club member amenities, club member social events, scholarships to worthy students, and other more appropriate uses of those dues which are supposed to be specifically geared toward actual club membership.

|

April 23, 2020:

The following is excerpted from the Synopsis and Commentary of the April 16, 2020 Board Meeting, during the Second Residents' Input Session, on this topic:

Sylvia Hechtman: Can you tell me why clubs need to pay for any improvements to the common area? Pickleball Club and Tennis Club are just like any other area; it’s the responsibility of the whole community to do it.

[Editor’s note: we concur wholeheartedly; see our comments above which we also posted on this news site under HOA Issues, under the sub-page on Awnings.]

Richard Greene: They volunteered.

[Editor’s note: Did they really? Or was this concocted between the leadership of those clubs and some board members who behind the scenes made it crystal clear that ponying up the dough would result in a favorable resolution? We suggest that that is exactly what happened based on what Richard said next.]

Richard: They wanted to make sure; it was possible they would not get it, the canopies, so they made the contribution to guarantee it.

[Editor’s note: Wait a moment: stop the presses! Per Richard, “they made the contribution to guarantee” a favorable board vote. How would the club leadership know this? Which board member assured them of this outcome? That sounds like a classic quid pro quo. This also sounds like a de facto shakedown: take your club dues and pay for this or we might vote it down; if you pay, we guarantee we will approve it. This is exactly what he is saying, folks. It is clear from this exchange that the leadership teams of the clubs got together with one or more board members and orchestrated this scheme whereby club dues would be used to grease the wheels and do the deals.

Who planted the seed for this scheme? How did the leadership teams even come up with the idea to pay for these HOA common area obligations with club money? Recall that the emails from the leadership teams clearly stated that they were trying to obtain “good will” with the Board (see the Awning page on this news site under the HOA Issues page for the emails). The Board represents the owners and owes the owners a fiduciary duty and to always act with good will, not the other way around. It is utterly unnecessary and improper to try and buy the Board’s good will when they already owe that to the community.]

Richard: No one asked them. They’re getting the benefit of it. It doesn’t mean that someone that’s not a member can’t utilize it.

[Editor’s note: And non-resident guests can utilize it, too, Richard, so why is club money even accepted for this common area amenity? And you say, “no one asked them?” How did they find out about it and how did they come up with the dollar amounts to offer? And how did they know that the Board meeting was occurring on Thursday instead of the usual Wednesday? And you further say, “they’re getting the benefit of it” but in fact they are not getting the benefit for themselves alone; they are in fact relieving the Board of its obligation to the HOA at large.

The Board should have more rightly rejected these improper offers, whether they germinated with the leadership team(s) or whether they germinated from a Board member who suggested it to the leadership team(s). This was the Board’s error or incompetence in finalizing the measurement of the canopy. More likely than not, this germinated directly from the Board, because the awning company surely did not contact the club leadership; they would have contacted the property manager, or the property manager would have contacted the awning company and worked in conjunction with the Board to deal with the issue of the improper measurement.]

Sylvia Hechtman: Why couldn’t it go to the Board first? I’m concerned that you’re setting a precedent.

[Editor’s note: Excellent two points in Sylvia’s last two sentences. The Board should immediately put this back on the Agenda to rescind and correct this dangerous precedent. No club moneys should be accepted for a common area expense: it promotes the exact type of wheeling and dealing behind the scenes that is unfair to the community at large and creates an underground sub-culture where special interests cozy up to board members and offer money to offset pet projects. Taking this money incentivizes and promotes this behavior, and sets a very dangerous precedent that if you have money to offer the Board, your pet project will pass.

This sounds like classic vote-buying. Here are the statutes on commercial bribery; we are specifically not stating that this conduct falls within the statute, as we leave that for Florida lawyers and judges to decide [emphasis supplied in red]:

“838.15 Commercial bribe receiving.—

(1) A person commits the crime of commercial bribe receiving if the person solicits, accepts, or agrees to accept a benefit with intent to violate a statutory or common-law duty to which that person is subject as:

(a) An agent or employee of another;

(b) A trustee, guardian, or other fiduciary;

(c) A lawyer, physician, accountant, appraiser, or other professional adviser;

(d) An officer, director, partner, manager, or other participant in the direction of the affairs of an organization; or

(e) An arbitrator or other purportedly disinterested adjudicator or referee.

(2) Commercial bribe receiving is a third degree felony, punishable as provided in s. 775.082, s. 775.083, or s. 775.084.

History.—s. 1, ch. 90-301.

838.16 Commercial bribery.—

(1) A person commits the crime of commercial bribery if, knowing that another is subject to a duty described in s. 838.15(1) and with intent to influence the other person to violate that duty, the person confers, offers to confer, or agrees to confer a benefit on the other.

(2) Commercial bribery is a third degree felony, punishable as provided in s. 775.082, s. 775.083, or s. 775.084.”

Richard: We didn’t want to lose the discount. The vendor had a customer, and that’s why the vote was taken when it was.

[Editor’s note: Mierda de toro.]

[Editor’s further note: In northern Mexico and the southwestern United States (particularly California), the phrase mierda de toro(s) (literally "shit from bull(s)") is used often as a Spanish translation of bullshit in response to what is seen by the Spanish speaker as perceived nonsense. Citation: Hamer, Eleanor; Diez de Urdanivia, Fernando (2008). The Street-Wise Spanish Survival Guide: A Dictionary of Over 3,000 Slang Expressions, Proverbs, Idioms, and Other Tricky English and Spanish Words and Phrases Translated and Explained. Skyhorse Publishing. ISBN 978-1-60239-250-2.

If the Board is now claiming that there was an urgency about losing a supposed discount on a second canopy that was never on any Board Agenda to being with, but appeared out of thin air because of the Board’s incompetence, then this community has been snookered again, and the Board now wants to rob the piggybanks of the clubs to lessen the impact of the Board’s error and/or its incompetence. The onus of that error was on the Board, regardless of who made the error, because the buck stops with the Board, and the club leadership should not have been exclusively privy to that issue. If the Board signed a contract and there was an error, the Board on behalf of the HOA is obliged to correct that error, and not rely on or accept club money to offset that error, regardless of where or how that error germinated, because ultimately it was the Board that signed the contract. The Board has no right to use the club monies as a piggybank to fix its mistakes.

And further, Richard, when you stated that “they made the contribution to guarantee it” you proved that there was collusion behind the scenes, which was done between one or more board members and team leaders without the knowledge of or participation of the club memberships or the HOA members at large. The only way that the club leadership would have even known about the approximate dollar amount necessary to buy the awnings were if the details were shared with them by one or more board members. Why was that done?

Somebody at some point suggested a scheme whereby funds would be used by the clubs to subsidize these expenditures. Furthermore, recall that the club leadership was initially going to spend the clubs’ moneys without taking it to a member vote until they were called out about their improper attempt to raid the clubs’ piggybanks by this news site and others. That essentially forced the vote and even the ballot was manipulatively dishonest as we have previously pointed out on the Awning sub-page to the HOA Issues page on this news site.

To be clear, when the club leadership got caught, and they were forced to put the matter to a club vote, the “vote” itself was skewed as described in detail on the Awning page elsewhere on this news site. For example, the Pickleball “no” vote was phrased, “No – I do not want the Pickleball Club to contribute. I do not want the canopy.” Mierda de toro again (see translation and description above). In truth, the “no” vote was whether club funds should subsidize a canopy, not that the member did not want the canopy. Your Roving Reporter voted no for the club subsidy even though he is in favor of a canopy at the pickleball courts because he was getting tired of constantly raising and lowering the two umbrellas due to sun and rain and because it is a good investment for the betterment of the community. Your Editor also voted no to the club subsidy but also supported having a canopy there even though she has never raised or lowered the umbrellas due to personal height restrictions.

This shameful process is not leadership, and it is deceitful, manipulative, and dishonest. And if there were such a concern about losing a “discount,” what discount is being referred to, the fact that they are selling the HOA a second awning at a reduced price because the Board gave them the wrong measurements? Why not at least shop it for bids? And how did the club leadership find out about that anyway? And the second awning was never part of any prior Agenda item. The entire scenario doesn’t pass the sniff test. Welcome to business as usual at Cascade Lakes; buyer beware.

And lest there be no misunderstanding, again, we here at the news site believe that there should be a canopy at the pickleball courts; that is something that could have easily been added to any Agenda at any time and could have been properly dealt with at any of the bimonthly board meetings.

We repeat the last part of our comments above targeting the tennis and pickleball clubs:

It is obvious that the dues required for club membership are way too high, since apparently the clubs have thousands of dollars to spend on common area improvements, as opposed to club member amenities, club member social events, scholarships to worthy students, and other more appropriate uses of those dues which are supposed to be specifically geared toward actual club membership.]

Sue Leonard: Our leadership team is made up of active members in the community… [talked about all the different clubs and committees where the leadership team members are involved] …We are offering our help and support where we can. There is nothing more to it than that.

[Editor’s note: There’s a heck of a lot more to it than that. Nice spin on attempting to justify it, Sue, but we’re not buying what you’re selling, and your statement has nothing to do with the impropriety of what you actively participated in doing behind the scenes. Your statement, along with your leadership team’s email pining for good will toward the Board, also proves that the Board went to you and your well-connected group of insiders to create this scenario because otherwise you would not have known about it. The Board willingly used you and your team to get club funds to cover their incompetence.

Here is the definition of “opportunist” from the Oxford Dictionary: “a person who exploits circumstances to gain immediate advantage rather than being guided by consistent principles or plans.” The Board, like true opportunists, suckered you, your pickleball leadership team, and the tennis club leadership team into wresting club funds away from true and proper club expenditures and instead snookered you into using club funds to pay for the Board’s error and incompetence. Here is what the Board essentially said to you: you’ll get your awning if you pony up $1,000, and tennis club, for good measure you get to kick in $2,000, and we’ll call it a donation. Simply put, Sue, you’ve been played.

The Board did a great job negotiating with club leadership teams to get money for this HOA obligation incurred by the Board’s incompetence. Too bad they don’t use these negotiating skills to negotiate with vendors on the big contracts to save the community hundreds of thousands of dollars, as opposed to the $3,000 they saved by conning you and the clubs.

The leadership teams and the Board are all very proud of themselves for their supposed accomplishment of getting two canopies in this manner. Rather, they should all be ashamed of themselves. You all sold out the clubs for a lousy $3,000 to an HOA Board which has a budget in the millions and which in a free-wheeling way decided to spend $130,000 on a shed without a community vote (see Shed sub-page under the HOA Issues page on this news site). This is only the second board meeting of the new Board and it is, once again, keeping this news site very busy.]

|

April 26, 2020:

Acceptance of Club Funds to Subsidize the HOA is a Taxable Event:

Per IRS rules, an HOA’s quarterly dues and special assessments, which constitute revenue to the HOA, are nevertheless not subject to the 30% tax rate otherwise applicable to other monies received by the HOA. Those specific revenue sources are specifically exempted from the federal tax otherwise due on other revenue sources received by an HOA per 26 U.S. Code Section 528(d)(3).

Any monies expended on HOA matters, which includes HOA common area improvements, must be made on a proportionate basis to all members, i.e., derive from quarterly dues or special assessments, to avoid tax consequences on moneys received and ultimately used for any HOA purpose. In other words, all incoming funds used for HOA matters, which necessarily includes common area improvements, must be paid for proportionately by the membership in order to avoid tax liability at the HOA rate of 30%, and the only way that that is accomplished is via quarterly dues and special assessments. To be clear, these revenue sources, i.e., quarterly dues and special assessments, are proportionate and equally shared and contributed to by owner/members. The acceptance of quarterly dues and special assessments are specifically not taxable events per IRS rules governing HOAs [26 U.S. Code Section 528(d)(3)].

The HOA took in $3,000 in revenue from non-HOA proportionate sources to subsidize itself (in this case, club monies from the tennis club and the pickleball club, both separate and independent corporations, but the rule applies to any revenue sources). None of that money was part of either quarterly dues or a special assessment, and therefore none of it was a proportionate contribution from the member/owners. Therefore, per IRS rules, it appears that receiving this revenue produced a taxable event, because it was revenue taken from non-exempt sources.

Taking monies from non-HOA sources (in this case, from two separate and distinct corporations, but in any case), and using that non-HOA, non-exempt money to subsidize the HOA, with said HOA in turn then purchasing awning for common area improvements per a contract between the HOA and the awning company, and thus getting the benefit and value therefrom, constitutes a revenue-producing activity; those amounts are therefore taxable on IRS Form 1120-H at the standard 30% rate for HOAs.

Therefore, that $3,000 that the HOA earned from the club contributions is taxable in the amount of $900 (30% of $3,000), and the HOA needs to account on its financial books for the additional $900 it now owes the IRS as part of the cost of the awnings. How is it fiscally responsible to have some individuals (in this case through two distinct corporations) disproportionally pay for HOA obligations and/or improvements which in turn generates a taxable event to the entire HOA? Answer: it most certainly it not.

The Treasurer of this HOA referred to these monies as a “donation.” This was not a donation, however, because the Treasurer admitted that the clubs received a “benefit” for their contributions, as described previously on this news site; rather, it was a profit generating activity which resulted in the enrichment of the entire HOA, thus creating a taxable event. Even if it were construed to be a donation, which this subsidy clearly was not, the HOA would still have to pay taxes on the revenues it received because it received a financial benefit from those non-HOA, non-exempt monies which were neither quarterly dues nor special assessments.

The finagling of the awning invoices/payment methodology to effectuate this scheme may expose the homeowners to IRS penalties and interest if an audit were undertaken and this anomaly were discovered. It may also red flag the HOA for future IRS audits, which would be very costly. This is not fiscal responsibility, and it is therefore incumbent upon the Board to immediately place on the next Agenda a motion to rescind acceptance of these club monies to protect the members of this HOA, or alternatively, to set aside an additional $900 in HOA funds to pay this tax obligation, the latter of which was caused by a lack of fiscal responsibility in the first place and is an unnecessary additional cost to the HOA.

|

May 14, 2020:

Re: HOA Taxable Event: Taking Money for Awnings

The following exchange occurred with respect to our above post concerning the taxable event created when the HOA took money from the clubs for the purchase of the sports center awnings. We have removed the resident’s identity and replaced it with the word “Anonymous.” The resident challenged our post, to which we invited the resident to explain why our post was not accurate, and the following interesting exchange occurred (we have edited out parts of the emails that had nothing to do with the issue, but otherwise we have posted the emails unedited):

Anonymous wrote:

Hello Vicki

…

Oh, perhaps I should mention that your posting about our HOA being subject to income tax was pretty much inaccurate.

Have a good day.

Anonymous

We replied:

Hi, Anonymous,

...

If you believe that the post on the taxable nature of the club monies taken by the BOD on behalf of the HOA is "pretty much inaccurate," please explain on what basis you make that assertion, as we are always willing to be educated. The IRS rules and guidelines were pretty clear and we made sure to read them on the subject before posting that article.

Cordially,

Vicki and Arthur

CascadeLakesResidents.com

Anonymous wrote in response:

Ok, but I’ll be quite brief.

First, I see nothing disallowing a club, whose members are all members of our HOA, not be permitted to make a capital contribution to the HOA. (hence, no taxable income). It could be easily argued that this is permissible. For example, there is case law regarding a municipality contributing money to a developer in order to facilitate the creation of a park within the development. Held, a capital contribution and not taxable. I realize that the developer was not an HOA, but it’s the same principal.

Second, even if it were Non-qualified income, the HOA is permitted to recognize certain non-qualified expenses, to defray the income. This is explained in regulation as well as form instructions which mention that, for example, an HOA’s management fees can be apportioned in some reasonable manner, against income. Also, direct HOA expenses, such as legal fees, to earn the income can be deducted. Other HOA expenses would be subject to apportionment. It would be quite easy to allocate a sufficient amount of expenses to (more than) wipe out the income.

Third, to be technical, even if the donation were Non-qualified income and and it had no expenses to offset the income, it still may utilize a $100 “standard deduction”. Not much different from your numbers, but nonetheless a difference.

This exercise would never get to my third point: just mentioned to be accurate.

Even if all my points Above were wrong, this activity would never be audited by IRS based on the size of the income.

The IRS, although not acting in a reasonable fashion all the time, does try not try to raise issues which would both take time and, if successful, result in an assessment of practically nothing.

Anonymous

We wrote in response:

Hi, Anonymous,

Thanks for your email. We appreciate that you have taken the time to write in response to our post on the subject of the taxable nature of the monies the HOA Board accepted from the independent tennis and pickleball clubs for partial payment of the community’s awnings.

In response, we will also try to be brief but will endeavor to address each of the points you have raised.

- Contrary to your claim, not all club members are in fact members of our HOA. Renters and ringers who pay club dues are not HOA members.

- The fact that most of the club members are members of the HOA is irrelevant. These are two separate and independent corporate entities registered with the Department of State.

- These funds are not capital contributions to the HOA by definition by virtue of the facts stated above in numbers one and two.

- HOA rules are specific and the rules regarding municipalities and developers are completely separate and have no precedential value to the issue at hand. Arguing case law concerning municipalities and developers would not impress the IRS, its Office of Appeals, or the United States Tax Court.

- There is nothing wrong with having expenses against income, but that does not excuse the requirement to declare the income. Most of your comments entail the use of deductions against income, but the funds are still declarable income.

- HOA expenses are to be paid by the HOA as a whole. Characterizing it against the influx of this income is also irrelevant and does not affect the requirement of declaring the income.

- You state that management fees can be apportioned against income in some reasonable manner. How so? Management fees are paid against non-income quarterly dues and special assessments, just like landscaping, attorneys fees, and the like.

- What expenses are you suggesting would wipe out this income that are not covered by the quarterly dues and special assessments? And even if these unidentified expenses wipe out the income as you suggest, that still does not excuse the failure to declare the income. There are lines on the form for income, lines for deductions, and additional statements that can be added to the return with additional deductions and explanations. None of this changes the fact that this is declarable income.

- Your mention of a $100 standard deduction does not make sense to us here. Again, if there is a permissible deduction, then by all means the taxpayer has the right to utilize it. It has no bearing, however, on the obligation to declare the income.

- The IRS chooses to audit based on a number of factors, and if there were an audit for a reason other than what we have raised, the fact that this, too, was not declared would raise an additional red flag and might cause the IRS to look more carefully at other areas of the return. There is no reason to deliberately fail to include income on a return and invite scrutiny unnecessarily. Pure and simple, it is dishonest, and it is fiscally irresponsible for the Board to put the association at risk no matter the amount of the outside income it collects.

Now, if any of the above facts are inaccurate, please let us know, so that we can educate ourselves further.

We will be posting your comments and our response on our news site. Please advise if you wish that your comments be posted anonymously as opposed to identifying you by name. If you feel strongly about your position, there should be no reason to hide your identity, but we will honor your wishes if you desire anonymity.

Best regards,

Vicki Roberts, Editor and

Arthur Andelson, Reporter

[Editor’s note: we did not receive any response to our last email.]

|

|